Prohibition of Acceptance of Deposits by Unincorporated Bodies

|

Prohibition of Acceptance of Deposits by Unincorporated Bodies

(Governed by S. 45S of the Reserve Bank of India Act, 1934)

| 1. Who can borrow |

Circumstances |

From whom? |

| Individual & Firm |

1. a) If his/its business wholly/partly includes any activities specifiedin S. 45I(c) OR

- If his/its principal business is receiving deposits under any scheme/arrangement/manner or lending in any manner.

|

Only from his relatives or relatives of any partner but not from partner(s). |

| |

2. In any other case. |

Any person. |

| Unincorporated association of individuals |

1. If engaged in business specified above. |

No one. |

| |

2. In any other case. |

Any person. |

The position applicable from 01.04.1997 is as follows:

- Deposit is defined to include any receipt of money by way of deposit or loan or in any other form, but excludes amounts :

| Received as way of |

Received from |

Received by |

| a) Share Capital |

a) Any banking co. including Scheduled/ Co-operative Bank

|

Subscription to a client’s fund |

| b) Partners Capital |

b) IDBI/SFC/Specified financial institution under IDBI Act/RBI Act |

|

| c) Security/Earnest Money/Advance against

orders |

c) Individual/firm/AOP not being a body corporate registered under any money lending enactment |

|

| d) Credits in the account on Sale of property |

|

|

- Deposits held as on 1.4.1997 not in accordance with (1) above, shall be repaid immediately when due or within 3 years from 1.4.1997 whichever is earlier. RBI, on application may extend this period by not more than 1 year, specifying any conditions.

- On and from 1.4.1997, no person referred to in (1) shall issue or cause to be issued any advertisement in any form for soliciting deposit.

- Activities contained in S. 45I(c) are Financing (Loans etc.); Investment (Shares, debentures, etc.); Hire Purchase; Insurance, Chit-fund or Kuries; Collecting and disbursing moneys in any manner under any scheme/arrangement.

But does not include if principal business is that of agricultural operations, industrial activities, purchase/sale of goods (not securities) or providing services, purchase, construction/sale of immovable property.

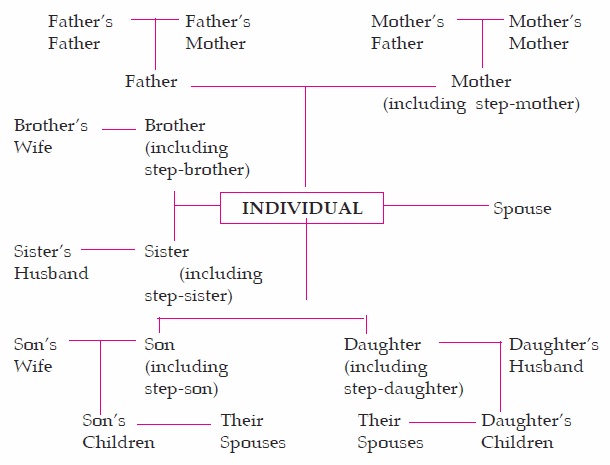

- For the above purpose, a person shall be deemed to be a relative of another, if they are :

- Members of an HUF;

- Husband and wife;

- Related in the manner indicated in section 6(c) of the Companies Act, 1956 as under :

Back to Top

|