Share capital, Debentures and Issue of Securities

(1) Kinds of share capital [S. 43] and their voting rights [S. 47(1)]

| |

Equity Share Capital

|

Preference Share Capital

|

|

Share Capital [S.43]

|

- With voting rights

- With differential rights as to dividend, voting or otherwise in accordance with the prescribed rules

|

means that part of the issued share capital of the company which carried or would carry a preferential right with respect to –

- Payment of dividend; and

- Repayment, in case of winding up or repayment of capital

|

|

Voting rights

[S. 47(1)]

|

- No voting rights in respect of payment of calls in advance

- On show of hands – 1 member = 1 vote; and

- on a poll – in proportion to his share in the paid-up equity share capital of the company

|

- Every member holding preference share capital shall have a right to vote only on

- the resolutions placed before the company which directly affect the rights attached to his preference shares and,

- any resolution for winding up of the company or for repayment orreduction of its equity or preference share capital

and his voting rights on a poll shall be in proportion to his share in the paid-up preference share capital of the company

- Further voting rights of equity shareholders : voting rights of preference shareholders = paid up equity share capital : paid up preference share capital

Example:

Paid-up Equity share capital: ₹ 700

Paid-up Preference share capital: ₹ 300

Voting right of a Preference shareholder holding ₹ 100, on a poll to repay ₹ 200 to equity shareholders

= 100 / 300 * (300/(700+300))

- If dividend in respect of any class of preference shares has not been paid for 2 years or more, such preference shareholders shall have a right to vote on all the resolutions placed before the company.

|

(2) Publication of Authorised, Subscribed and paid-upcapital (S. 60)

|

If any notice, advertisement or other official publication, or any business letter, bill head orletter paper of a company contains a statement of the amount of the authorised capital of the company

|

→

|

it shall also contain a statement, in an equally prominent positionand in equally conspicuous characters, of the amount subscribed and paid-up capital of the company.

|

(3) Types of Issue of Securities – an overview

|

Sr. No.

|

Types of issue of securities

|

Private Company

|

Public Company

|

|

(i)

|

Rights Issue [S.62(1)(a)]: Board resolution

to equity shareholders of the company in proportion, as nearly as circumstances admit, to the paid-up share capital on those shares

|

✓

|

✓

|

|

(ii)

|

Employees’ Stock Option Scheme[S.62(1)(b)]: Special resolution to employees

|

✓

|

✓

|

|

(iii)

|

Any person [S.62(1)(c)]: Special resolution

(a) Private Placement [S.42, R.14 of PSR]: Refer (6) & (7) below

incl. Preferential allotment [R.13 of SCDR]to:

– To Shareholders only

– To Others

|

|

|

|

✓

|

✓

|

|

(b) Public Offer [Part I of Chapter III]:

|

☓

|

✓

|

|

(c) Sweat Equity shares [S.54]: Refer (8) below

|

✓

|

✓

|

|

(iv)

|

Bonus Issue [S.63(1), R.14of SCDR]: Special resolution

Issue of fully paid-up Bonus Shares to its members in any manner, out of:

Free reserves / Securities Premium Account / Capital Redemption Reserve

|

✓

|

✓

|

(4) Application of premium received on issue of shares [S. 52]

- Issue of unissued shares of the company to the members of the company as fully paid bonus shares;

- Writing off the expenses of, or the commission paid or discount allowed on, any issue of shares or debentures of the company;

- Purchase of own shares or other securities u/s. 68 (buy-back of securities);

In case of companies as may be prescribed and whose FS comply with AS prescribed for such class of companies u/s 133, Premium received on issue of shares can also be applied for the following:

- Premium payable on the redemption of any redeemable preference shares or of any debentures of the company;

- Writing off the preliminary expenses of the company.

(5) 2Prohibition Issue of shares at Discount [S.53]

Any share issued by a company other than Sweat Equity Shares at a discounted price shall be void.

(6) Private placement vis-→-vis Preferential Offer

|

Private placement means

|

Preferential Offer means

|

|

any offer or invitation to subscribe or issue of securities

|

an issue of shares or other securities

[i.e. equity shares, fully convertible debentures, partly convertible debentures or any other securities, which would be convertible into or exchanged with equity shares at a later date]

|

|

to a select group of persons

|

to any select person or group of persons on a preferential basis

|

|

by a company

|

by a company

|

|

(other than by way of public offer)

[by its nature, it also does not include rights issue, employee stock option scheme, employee stock purchase scheme or an issue of sweat equity shares or bonus shares or depository receipts issued in a country outside India or foreign securities]

|

does not include shares or other securities offered through a public issue, rights issue, employee stock option scheme, employee stock purchase scheme or an issue of sweat equity shares or bonus shares or depository receipts issued in a country outside India or foreign securities

|

|

through private placement offer-cum-application

|

|

|

which satisfies the conditions specified in S.42

|

|

|

Private placement need not necessarily be Preferential Offer

|

Preferential Offer must be Private placement

|

(7) Private Placement[S.42, R.14 of PSR]

Private placement is one of the most common modes of raising funds by way of issue of shares. It, inter alia, involves the following:

|

Conditions precedent

|

- the allotments with respect to any offer or invitation made earlier have been completed or that offer or invitation has been withdrawn or abandoned by the company .[S.42(3), R.14(2)(b)]#

- previously approved by the shareholders by a Special Resolution, for each of the Offers or Invitations[R.14(2)(a)]

- special resolution only once in a year sufficient for all the offers or invitation for non-convertible debentures during FY

- the basis or justification for the price (including premium, if any) disclosed explanatory statement annexed to the notice for the general meeting

- offer of securities or invitation to subscribe securities to persons not > 200, (excluding QIBs, and employees of the company being offered securities under ESOS as per section 62(1)(b)), in a FY (reckoned individually for each kind of security that is equity share, preference share or debenture). [S.42(2), R.14(2)(b)]#

#Not applicable to NBFCs / HFCs registered with RBI / NHB respectively if they are complying with regulations made by RBI / NHB in respect of offer or invitation to be issued on private placement basis

|

|

3Offer

|

- Made through issue of a private placement offer letter in Form PAS-4

- accompanied by an application form serially numbered and addressed specifically to the person to whom the offer is made –

- sent to him, either in writing or in electronic mode, within 30 days of recording the names of such persons in accordance with S.42(7). [S.42(1), R.14(1)(a) & (b)]

- All offers covered under S.42 shall be made -

- only to such persons whose names are recorded by the company prior to the invitation to subscribe, and

- such persons shall receive the offer by name, and

- a complete record of such offers shall be kept by the company in Form No. PAS-5 and

- a copy of such record in PAS 5 along with PPOL in Form PAS-4 to be filed with the RoC within 30 daysof circulation of relevant PPOL.[S.42(7)]

- Not to release any public advertisements or utilise any media, marketing or distribution channels or agents to inform the public at large about such an offer.[S.42(8)]

- investment size not to be < ₹ 20,000 of face value of the securities [R.14(2)(c)]# (see Note at Conditions Precedent above)

|

|

Payment of subscription money

|

- payment for subscription to securities shall be made from the bank a/c of the person subscribing to such securities [R.14(2)(d)]

- in case of joint holders, it shall be paid from the bank account of the person whose name appears first in the application

- The Co shall keep the record of the Bank a/c from where such payments for subscriptions have been received –

- 4All monies payable towards subscription of securities on private placement basis under S.42 shall be paid through cheque/ demand

draft / other banking channels but not by cash [S. 42(5)]

- Monies received on application u/s 42 shall be kept in a separate bank account in a scheduled bank and shall not be utilised for any purpose other than—

- for adjustment against allotment of securities; or

- for the repayment of monies where the company is unable to allot securities.

|

|

Post offer closure compliances

|

|

(8) Issue of Sweat Equity Shares [S. 54]

|

Meaning [S.2(88)]

|

“sweat equity shares” means such equity shares as are issued by a company to its directors or employees at a discount or for consideration, other than cash, for providing their know-how or making available rights in the nature of intellectual property rights or value additions, by whatever name called

|

|

What can be issued [S.54(1)]

|

Sweat equity shares of a class of shares already issued

|

|

To whom it can be issued [R.8(1), Expl (i)]

|

directors or employees

- a permanent employee of the Co. who has been working in India or outside India, for at least last 1 year; or

- a director of the Co., whether a WTD or not; or

- an employee or a director as defined in sub-clauses (a) or (b) above of a subsidiary, in India or outside India, or of a holding company of the Co.;

|

|

Quantum [R.8(4)]

|

- Max (NOT > than 15% of the existing paid-up Equity Share Capital in a year, OR Shares of the Issue Value of ₹ 5 crores)

- not > 25% of the Paid-Up Equity Capital of the Company at any time.

|

|

Valuation [R.8(6)]

|

Price of equity shares shall be determined by a Registered Valuer as fair price giving justification for such valuation.

|

|

Lock-in [R.8(5)]

|

3 years from the date of allotment.

|

|

Conditions [S.54(1)]

|

- the issue authorized by a special resolution

- allotment to be completed within 12 months of

passing special resolution [R 8(3)];

- the resolution specifies the number of shares, the current market price,

consideration, if any, and the class or classes of directors or employees to

whom such equity shares are to be issued;

- at the date of such issue, not < 1 year has elapsed since the date on

which the Co had commenced business

- A startup Co may issue sweat equity shares not exceeding 50% of its

paid up capital up to 5 years from the date of its incorporation or

registration.

- where the equity shares of the Co are listed on a recognised SE, the

sweat equity shares are issued in accordance with the relevant SEBI

regulations.

|

|

Pari passu with other equity shareholders [S.54(2)]

|

The rights, limitations, restrictions and provisions as are for the time

being applicable to equity shares shall be applicable to the sweat equity shares

issued u/s. 54 and the holders of such shares shall rank pari passu with

other equity shareholders.

|

|

Accounting treatment and Managerial remuneration [R 8(6), (9), (10), (11), (12)]

|

|

sweat equity shares issued for a non-cash consideration on the basis

of a valuation report obtained from the registered valuer

|

|

where the non-cash consideration takes the form of a depreciable /

amortizable asset

|

Other cases

|

|

it shall be carried to the balance sheet of the Co in accordance with AS

- amount of the accounting value (fair value) of the Sweat Equity Shares

as determined a registered valuer under Rule 8(6) > the value of the asset

acquired as per the valuation report àè shall be treated as a form of

compensation to the employee / director in the FS of the Co

|

It shall be expensed as provided in the accounting standards

- if the Sweat Equity Shares are not issued pursuant to acquisition of an

asset àè accounting value of sweat equity shares shall be treated as a form

of compensation to the employee / director in the FS of the Co,

- if issued to any Director / Manager àè the amount of Sweat Equity Shares

issued shall be treated as a part of Managerial Remuneration

|

|

|

Disclosures

[R 8(13)]

|

Prescribed details are required to be disclosed in the Directors’ Report for

the year in which sweat equity shares are issued

|

|

Register of Sweat Equity Shares

[R 8(14)]

|

To be maintained in Form No. SH.3 at the registered office of the company or

such other place as the Board may decide

|

(9) Issue and Redemption of Preference Shares [S. 55]

|

Permitted to issue

|

- Redeemable preference shares only

|

|

Preconditions for issue [S.55(2), R.9(1)]

|

- Authorised by AoA

- authorized by passing a special resolution in the GM

- at the time of such issue of preference shares, the Co has no subsisting default in the redemption of preference shares issued either before or after the commencement of Co Act 2013 or in payment of dividend due on any preference shares

|

|

Tenure

[S.55(2), R 10]

|

- 20 years

- For infrastructure projects (specified in Schedule VI to the Co Act, 2013) : > 20 years, but NOT > 30 years

- Redemption of minimum 10% on an annual basis from 21st year at the option of preference shareholders

|

|

Redemption out of -

[S.55(2), 2nd proviso, R.8(4)]

|

- Profits available for dividend

- sum equal to the nominal amount of the shares to be redeemed out of such profits, be transferred to Capital Redemption Reserve A/c

- Proceeds of fresh issue of shares made for the purpose of such redemption

|

|

Premium on redemption, if any, to be provided before redemption of preference shares [S.55(2), 2nd proviso, (d)]

|

|

By such prescribed class of companies whose FS comply with AS prescribed for such class of companies u/s. 133

|

Other companies OR

|

|

premium, if any, payable on redemption of any preference shares issued on or before the commencement of Co Act 2013 by any Co

|

|

|

- Out of profits

- Out of Securities Premium A/c

|

|

|

Redemption of preference shares as per its terms [R.8(6)]

|

- at a fixed time or on the happening of a particular event;

- any time at the company’s option; or

- any time at the shareholder’s option

|

(10) Reduction of share capital [S. 66]: An overview

Meaning and Purpose: Reduction of share capital means the reduction of issued, subscribed and paid-up capital of the Company. The reduction of capital is mainly done by companies for producing a more efficient capital structure. To reduce its share capital, the Co should have the power under its AoA to do so. If the AoA do not contain any provision for reduction of capital, then the AoA must first be altered so as to give such power and then the special resolution for reducing capital should be passed.

|

Sr. No.

|

Modes of reduction

|

Section

|

|

(A)

|

extinguish or reduce the liability on any of its shares in respect of the share capital not paid-up

Example:

Face value: ₹ 10

Paid-up value: ₹ 7

Extinguish / reduce the liability to pay balance ₹ 3

|

66(1)(a)

|

|

(B)

|

either with or without extinguishing or reducing liability on any of its shares,—

(i) CANCEL any paid-up share capital which is lost or is unrepresented by available assets;

Example:

Paid up capital: ₹ 10

Accumulated losses: ₹ 7

Paid up capital to the extent of ₹ 7 be cancelled to write off Accumulated losses of ₹ 7

or

(ii) PAY OFF any paid-up share capital which is in excess of the wants of the Co, alter its memorandum by reducing the amount of its share capital and of its shares accordingly:

Example:

Paid up capital: ₹ 10

Excess capital not required by the Company: ₹ 4

Paid up capital to the extent of ₹ 4 be returned (paid in cash) to the shareholders.

Provided that no such reduction shall be made if the Co is in arrears in the repayment of any deposits accepted by it, either before or after the commencement of Co Act 2013, or the interest payable thereon.

|

66(1)(b)

|

|

(C)

|

Application of PREMIUMS RECEIVED ON ISSUE OF SHARES, otherwise than in the following manner:

|

52(1)

|

| |

|

by prescribed class of companies whose financial statement comply with the AS prescribed for such class of companies u/s 133

|

by Other companies

|

|

(a) towards the issue of unissued shares of the Co to the members of the Co as fully paid bonus shares;

|

(a) in paying up unissued equity shares of the Co y to be issued to members of the Co as fully paid bonus shares; or

|

|

(b) in writing off the preliminary expenses of the Co; -

|

—

|

|

(c) in writing off the expenses of, or the commission paid or discount allowed on, any issue of shares or debentures of the Co;

|

(b) in writing off the expenses of or the commission paid or discount allowed on any issue of equity shares of the Co; or

|

|

(d) in providing for the premium payable on the redemption of any redeemable preference shares or of any debentures of the Co; or

|

—

|

|

(e) for the purchase of its own shares or other securities under section 68.

|

(c) for the purchase of its own shares or other securities under section 68.

|

|

Clause (d) of 2nd proviso to S. 55(2)

|

|

(D)

|

Application of CAPITAL REDEMPTION RESERVE ACCOUNT, otherwise than in paying up unissued shares of the Company to be issued to members of the Co as fully paid bonus shares

|

Clause (c) of 2nd proviso to S. 55(2) & S. 55(4)

|

|

Broad procedure for Reduction

|

|

Board approval → Special resolution → Application to NCLT → * Certificate from the Auditor

to be filed with NCLT → NCLT order of confirmation of the reduction of share capital→ Filing of NCLT order with RoC

|

* the accounting treatment, proposed by the company for such reduction is in conformity with the accounting standards specified in section 133 or any other provision of the Co Act 2013

(11) Restrictions on purchase by company or giving of loans by it for purchase of its shares [S. 67]:

A private Co is exempted from the provisions of S. 67 if following conditions are fulfilled:

- No other body corporate has invested any money in its share capital;

- Borrowing from banks, FIs or anybody corporate is < (2 * its paid-up capital) or ₹ 500 million, whichever is lower; and

- It has not defaulted in repayment of such borrowings at the time of purchase of own shares.

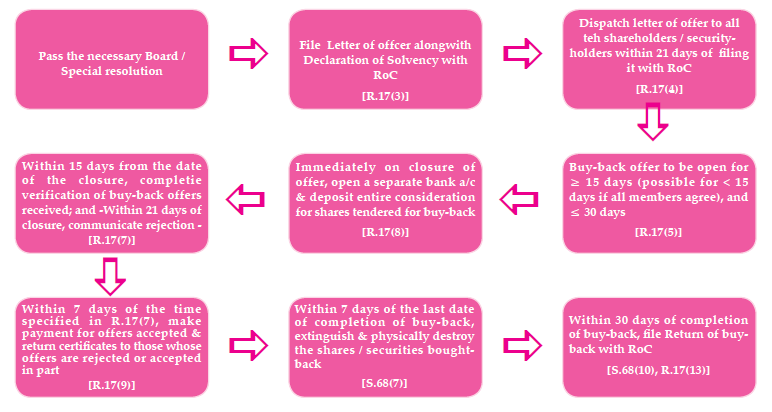

(12) Power to purchase its own shares (i.e. buy-back of securities) [S.68, R. 17]

Buy-back of own shares or other specified securities

|

Out of: (1)

|

- its free reserves;

- the securities premium account; or

- the proceeds of the issue of any shares or other specified securities, not being proceeds of an earlier issue of the same kind of shares or same kind of other specified securities

|

|

Conditions:

(2)

|

- authorised by its articles;

|

a special resolution has been passed at a GM of the Co authorising the buy-back

|

such buy-back has been authorised by the Board resolution passed at its meeting

|

|

buy-back is (>10%, and) < 25% of (paid-up capital + free reserves of the Co)

|

buy-back is < 10% of (paid-up capital + free reserves of the Co)

|

|

- buy-back is < 25% of (paid-up capital + free reserves of the Co)

|

- buy-back of equity shares (in number) in any FY < 25% of its total paid-up equity capital in that FY;

|

| |

- the ratio of (secured + unsecured debts owed by the Co after buy-back) is NOT > 2 * (the paid-up capital + free reserves) i.e. Debt-Equity ratio is NOT > 2:1:

- all shares / other specified securities for buy-back are fully paid-up;

- buy-back of listed shares or other specified securities is in accordance with the relevant SEBI

regulations ; and

- buy-back offer shall NOT be made within 1 year from the date of the closure of the preceding offer of buy-back, if any.

|

|

Disclosures on GM notice (3)

|

Notice of GM at which the special resolution is proposed to be passed for buy-back shall be accompanied by an explanatory statement giving specified disclosures.

|

|

Completion of buy-back (4)

|

Buy-back shall be completed within 1 year from the date of passing the relevant resolution

|

|

Modes of buy-back (5)

|

- from the existing shareholders /security holders on a proportionate basis;

- from the open market;

- by purchasing the securities issued to employees of the Co pursuant to a scheme of stock option or sweat equity

|

|

Declaration of solvency (6)

|

Before making such buy-back, file a declaration of solvency signed by at least 2 directors of the Co, one of whom shall be MD, if any, verified by an affidavit (formed an opinion that the Co will not be rendered insolvent within a period of 1 year)

|

|

extinguish the shares / securities bought-back (7)

|

extinguish and physically destroy the shares or securities so bought back within 7 days of the last date of completion of buy-back

|

|

Restriction of further issue of same kind of shares or other securities bought-back (8)

|

Co shall not make a further issue of the same kind of shares or other securities including rights issue (u/s 62(1)(a)) within 6 months of completion of buy-back except

- a bonus issue, or

- in the discharge of subsisting obligations such as conversion of warrants, stock option schemes, sweat equity or conversion of preference shares or debentures into equity shares

|

|

Register of

buy-back (9)

|

maintain a register of the shares or securities so bought in Form No. SH.10

|

|

Return of buy-back (10)

|

File with RoC within 30 days of completion of buy-back in Form No. SH.11

|

Broad overview of buy-back procedure of unlisted shares or securities

(13) Debentures [S. 71]

- Convertible Debenturescan be issued only when Special Resolution is passed for the same in the GM.

- No company shall issue debentures carryingvoting right.

- Secured Debenturescan be issued by a Co subject to terms and conditions prescribed in R.18(1) e.g. appointment of the debenture trustee before the issue of prospectus / letter of offer for subscription of its debentures, execution of debenture trust deed not later than 60 days after the allotment of the debentures. Such issue of debentures shall be secured by the creation of a charge on the properties / assets of the Co / its Sub Cos / its Hold Co / its Asct Cos, having a value sufficient for the due repayment of the amount of debentures and interest thereon.

- Date of Redemptionof secured debentures issued by :

- a company engaged in the setting up of infrastructure projects may >10 years but shall not >30 years shall not >10 years from the date of issue.

- any other company shall not >10 years from the date of issue.

- Conditions for appointment of Debenture Trustee are prescribed in R. 18(2).

- The Co shall create a DRRout of its profits available for payment of dividend as prescribed in R.18(7).

2 As per Co Amend Act 2017: (Addition) - Notwithstanding anything contained in sub-sections (1) and (2), a company may issue shares at a discount to its creditors when its debt is converted into shares in pursuance of any statutory resolution plan or debt restructuring scheme in accordance with any guidelines or directions or regulations specified by the RBI under the RBI Act, 1934 or the Banking (Regulation) Act, 1949. – came

into force from 9 Feb. 2018

3 As per Co Amend Act 2017: the private placement offer and application shall not carry any right of renunciation – Not yet operative

4 As per Co Amend Act 2017: (Addition) - the company shall not utilise monies raised through private placement unless allotment is made and the return of allotment is filed with the Registrar in accordance with S. 42(8) – Not yet operative

5 As per Co Amend Act 2017: Return of allotment of securities be filed with the RoC within 15 days (earlier, 30 days) of allotment. In case of default, the company, its promoters and directors shall be liable to a penalty for each default of 1,000 per day during which such default continues but not > 25 lakhs. – Not yet operative

Back to Top

|