GST Returns

SALIENT FEATURES OF RETURN FILING PROCESS

- Mandatory Electronic Filing of returns

- By directly punching details of the GSTN portal [www.gst.gov.in]

- By using the offline return preparation utility provided by the GSTN portal

- By using return filing software solutions provided by GST Suvidha providers [GSP’s] or ASP’s

- Uploading of invoice level details of B2B supplies (including export supplies) and consolidated details of other supplies

- Revision of returns not permissible. However, rectification can be done in subsequent tax periods

- Regular taxpayers to upload details of outward and inward supplies and a monthly return

- Quarterly compliance for taxpayers who have opted for composition scheme

- Separate compliance forms for non-resident taxpayers, Input Service Distributor, Person liable for TDS or TCS and holders of UIN

- Furnishing of summary return in Form GSTR-3B where ever due date for filing GSTR-1 and GSTR-2 is extended. Details furnished in Form GSTR-3B shall be auto populated in Form GSTR-3 for

that period which shall be editable by the taxpayer

- Accuracy and Accounting discipline shall play a pivotal role in return compliance

TYPES OF RETURNS

Depending on the nature of compliance to be undertaken under the law various types of returns have been prescribed under the Rules. Types of return forms and related details are tabulated here under:

|

Form

|

Nature of Compliance

|

Periodicity

|

Due Date

|

Section/ Return Rule

|

|

GSTR-1

|

Furnishing details of outward supplies

|

Monthly / Quarterly1

|

10th2 of the next month

|

S. 37 Rule 59

|

|

GSTR-2

|

Furnishing details of inward supplies

|

Monthly

|

15th3 of the next month

|

S. 38 Rule 60

|

|

GSTR-3

|

Return by regular taxpayer

|

Monthly

|

20th3 of the next month

|

S. 39(1)

Rule 61

|

|

GSTR-3B

|

Summary return

|

Monthly

|

To be furnished whenever there is an extension in time limit for filing GSTR-1 & 2 as per conditions provided in notification

|

Rule 61(5)

|

|

GSTR-4

|

Return by a taxpayer opting for composition

|

Quarterly

|

20th of the month succeeding the quarter

|

S. 39(2)

Rule 62

|

|

GSTR-5

|

Return for non-resident taxable persons

|

Monthly

|

20th of the next month4

|

S. 39(5)

Rule 63

|

|

GSTR-5A

|

Details of supplies of OIDAR services provided by person located outside India to a non-taxable in India

|

Monthly

|

20th of the next month

|

Rule 64

|

|

GSTR-6

|

Return for Input Service Distributor

|

Monthly

|

13th of the next month

|

S. 39(4)

Rule 65

|

|

GSTR-7

|

Return of Tax Deduction at Source [TDS]

|

Monthly

|

10th of the next month

|

S. 39(3)

Rule 66

|

|

GSTR-8

|

Statement of TCS by e-Commerce Operator

|

Monthly

|

20th of the next month

|

S. 52(4)

Rule 67

|

|

GSTR-9

|

Annual return by a regular Taxpayer

|

Annual

|

31st December of the next financial year

|

S. 44

R. 80

|

|

GSTR-9A

|

Annual return by a composition taxpayer

|

Annual

|

31st December of the next financial year

|

S. 44

R. 80

|

|

GSTR-9B

|

Annual return by an e-Commerce Operator

|

Annual

|

31st December of the next financial year

|

S. 44

R. 80

|

|

GSTR-9C5

|

Annual reconciliation statement/Audited Accounts

|

Annual

|

31st December of the next financial year

|

S. 35(5)

R. 80(3)

|

|

GSTR-11

|

Inward Supply statement by UIN holders

|

Monthly

|

—

|

R. 82

|

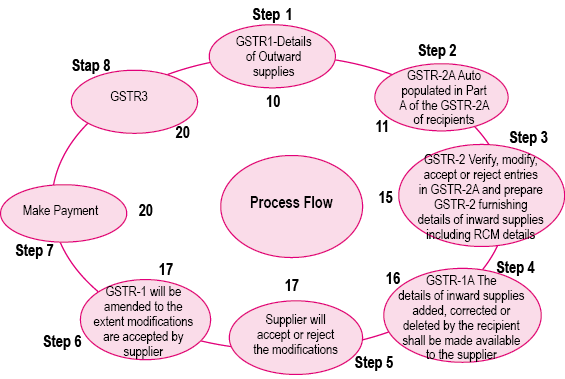

RETURN FILING PROCESS FLOW [GSTR-1, 2, 3]

FORM GSTR-1: DETAILS OF OUTWARD SUPPLIES MADE DURING A TAX PERIOD

[Sec. 37, Rule 59]

Broad Framework of the Form

The return filing process commences with the furnishing of details of outward supplies in Form GSTR-1. The broad architecture of Form GSTR-1 comprises of furnishing invoice level details and other details of outward supplies. Broad details that need to be furnished in Form GSTR-1 are enumerated hereunder:

- Details to be furnished include deemed supplies [made without consideration] in terms of Schedule I to the CGST Act, 2017

- Invoice level details of B2B Taxable Outward Supplies [Intra-State and Inter-State]

- Invoice Level details of B2C Inter-State Taxable Outward Supplies [where invoice value > ₹2.5 lakh]

- Invoice level details of zero rated supplies

- Consolidated details of B2C Taxable Outward Supplies [Intra-State and Inter-State]

- HSN wise summary of outward supplies

- Details of various documents issued

DATA TABLES IN FORM GSTR-1

|

Table

|

Particulars

|

Comments/ Remarks

|

|

1

|

GSTIN of the taxpayer

|

Shall be auto-populated on login

|

|

2

|

Legal Name and Trade Name of the taxpayer

|

Shall be auto-populated on login

|

|

3(a)

|

Aggregate turnover of preceding financial year

|

To be provided in first year

[Shall be auto-populated in subsequent year]

|

|

3(b)

|

Aggregate turnover for April-June, 2017

|

Applicable only for the first month

|

|

4

|

Details of following B2B Taxable Outward Supplies [Inter and Intra-State] to registered taxable persons holding GSTIN:

- Taxable under forward charge

- Taxable under Reverse Charge Mechanism6[RCM]

- Made through an e-Commerce operator attracting TCS [e-Comm wise]

|

Broad details to be furnished are as under:

- Recipient’s GSTIN7/ UIN, Invoice details [Ratewise], taxable value, tax amount and place of supply [where it is different from the recipient]

- In case of supplies through E-Commerce Operator GSTIN of the Operator also shall be specified

|

|

5

|

Following Taxable Inter-State Outward Supplies to unregistered person [B2C] where invoice value8 is >

₹ 2.5 lakhs:

- Supplies other than through e-Commerce Operator

- Supplies through e-Commerce attracting TCS [Operator wise]

|

Details to be furnished include:

- Details similar to Table 4 to be furnished [except GSTIN]

- Place of supply field is mandatory

|

|

6

|

Details of Zero Rated supplies9 and deemed exports10:

- Direct Exports out of India

- Supplies made to SEZ Developer or unit in SEZ

- Deemed Exports

|

Details to be furnished include:

- GSTIN of the recipient [to be left blank in case of exports]

- Details of Invoice, Shipping Bill or Bill of Export

- Ratewise details of taxable value and amount of IGST/Cess [Tax amount to be “0” where the supply is under Bond/ LUT]

|

|

7

|

Details of B2C inter and intra-States taxable outward supplies to unregistered persons [B2C] not covered in Table 5 shall be covered in this table [Net of Debit/ Credit Notes]:

- Inter and Intra-State supplies [Including made through e-Commerce Operator]

- Separate summary of supplies made through e-Commerce Operator [included above] to be given separately

|

Details to be furnished include:

- Ratewise consolidated values11 and tax12 thereon

- Identify State in case of inter-State supplies

- E-Commerce Operator summary of supplies made through each such operator

|

|

8

|

Consolidated values of NIL rated, exempted and Non-GST supplies to be furnished in this table. Separate details to be furnished of B2B and B2C supplies [Classified into inter and intra-State]

|

|

9

|

- Details of amendments to B2B taxable outward supplies reported in Table 4 and 6 and B2C large invoices for earlier periods furnished in Table 5

- Credit and Debit notes [Original]

- Amendments to Original Debit/Credit Notes

|

Details to be furnished include:

- Revised Document details to be specified and tagged against original document No.

- Details of Original Credit/Debit notes also to be specified in this table giving reference to invoice against which the same has been issued

- Amendment to Debit and Credit notes to be made by tagging the same to original Debit or Credit note

|

|

10

|

Allows amendments relating to B2C supplies covered in Table 7 of earlier periods. Month wise revised details to be furnished in respect of each month where rectification is desired

|

|

11

|

Details of advances received and adjustment of advances against outward supplies [Inter-State and Intra State separately]:

- Advances received in the current month

- Adjustments of advances against which invoices issued during the current month

- Amendment to information furnished in Table 11 during earlier months

|

Details to be furnished include:

- Rate wise details of advances received towards Taxable Inter-State and Intra-State supplies

- Rate wise details of adjustment of advances against Tax invoices issued in the current month

- Identify place of supply [State name] in case of Inter-State supplies

- Amendments to details of advances/adjustments provided in earlier months which need correction

|

|

12

|

HSN wise value of outward supplies made during the period. HSN codes would be mandatory as under:

|

Annual Turnover in the preceding financial year

|

Number of Digits of HSN Code

|

|

Up to ₹ 1.5 Crores

|

NIL [Description of supply to be provided]

|

|

> ₹ 1.5 Crores > ₹ 5 Crores

|

2-Digits

|

|

> ₹ 5 Crores

|

4-Digits

|

|

|

13

|

The GST Law and the rules made thereunder require a taxpayer to issue number of documents for various purposes [E.g. Invoices, Credit note, Debit note, Receipt voucher]. This table requires the taxpayer to provide a quantitative summary of every document issued during the month.

|

FORM GSTR-2: DETAILS OF INWARD SUPPLIES OF GOODS OR SERVICES

[Sec. 38, Rule 60]

Form GSTR-2 requires furnishing details of all inward supplies received during a tax period. Details of inward supplies shall be prepared based on auto-drafted details made available in Form GSTR-2A. This process would require the taxpayer to first go through the herculean task of reconciling the auto drafted details with the details as per books of account. Tablewise details to be furnished in GSTR-2 are summarised hereunder:

|

Table

|

CONTENTS OF GSTR -2

|

|

3

|

Furnish details of taxable inward supplies from registered taxable person [B2B] other than RCM supplies [Inter and Intra State]. Details to be furnished shall include:

- Invoice level [Rate wise] details of taxable inward supplies received from registered taxable person [B2B Inward Supplies]

- The taxpayer also needs to identify following at invoice level in respect of each entry in this Table:

- Nature of supply – Inputs, Input Services or Capital Goods [including Plant and Machinery]

- ITC Eligibility – Identify invoices where ITC is ineligible [for e.g. blocked credits in terms of Sec. 17(5)]

- ITC available in current tax period – Identify amount of ITC available in the current period

- Place of Supply – Identify amount of ITC available in the current period

|

|

4

|

Details of following taxable inward taxable supplies liable for payment of tax under RCM to be furnished in this table:

- Received from registered taxable person being notified supplies u/s. 9(3)

|

Taxpayer needs to furnish following details

- GSTIN of supplier and rate wise invoice details

- Name of the State [Place of Supply]

|

- Received from unregistered person and liable for RCM u/s. 9(4)

- Import of services

|

- Nature of Supply – Inputs, Input services or Capital Goods [Select from drop down]

- Identify Ineligible ITC13

- Amount of ITC available

|

|

5

|

Details relating to supplies of Inputs or Capital Goods received on a Bill of Entry from:

- Direct Imports from outside India

- Received from a SEZ Unit

|

Details to be furnished are as under:

- GSTIN of Supplier [in case of imports GSTIN of the Taxpayer shall be mentioned]

- Bill of Entry details [No.14, Date & Value]

- Taxable Value [i.e. Assessable Value as per Customs]

- Details to be furnished Rate-wise

- Nature of Supply – Inputs, Input services or Capital Goods [Select from Drop Down]

- Identify ineligible ITC

|

|

6

|

Details of amendments to details furnished for earlier tax periods including details of Debit and Credit Notes relating to:

- Details of inward supplies furnished in Table 3 or Table 4

- Details of Imports furnished in Table 5

- Original Debit and Credit Notes

- Amendments to details furnished relating to Debit or Credit Notes

|

Details to be furnished are as under:

- Provide details of Original Invoice or Bill of Entry so as to Tag them to the amendments

- Provide revised details against each of the original document details

- For whichever sub-table correction is required furnish revised details by selecting the appropriate sub-table and month

|

|

7

|

Details of Composition, NIL rated, exempted and Non-GST Inward Supplies

Consolidated values of the above have to be furnished giving bifurcation of Inter/ Intra State inward supplies

|

|

8

|

Details of ISD Credit received

[Details shall appear in GSTR-2A from ISD’s GSTR-6]

Following details are to be furnished:

- ISD Credit document [ISD Invoice or ISD Credit Note]

- Levy-wise amount of ISD credit

- Amount of eligible ISD Credit

|

|

9

|

Details of TDS and TCS

[Shall be available in Form GSTR-2A on the basis of return filed by the deductor in Form GSTR-7]

- TDS – Gross amount and TDS amount [Levy-wise]

- TCS – Gross amount less sales return and TCS amount [Levy-wise]

|

|

10

|

This table requires furnishing following details:

- Advances paid towards RCM supplies and tax thereon

- Adjustments of invoices against advance paid in earlier periods

- Correction to Information provided in this table in earlier months

|

Details to be furnished:

Advances liable for RCM

Tax Rate, Advance paid, State name and tax amount [Levy-wise]

Adjustments of [For current month]

Same details as specified above

Amendments to details furnished earlier

Furnish details for entire month against the sub-table that requires correction

|

|

11

|

ITC reversal and reclaim shall be furnished

[To be added to output liability and details to be furnished by the Taxpayer]

Reversal to ITC would broadly include following situations:

- Non-Payment to supplier within 180 days [2nd proviso Section 16(2)(d), Rule 37(2)]

- ISD Credit distributed is in the negative15 [Rule 39(1)(j)(ii)]

- Pro-rata reversal of ITC on inputs or input services put to other than business use or used for exempted outward supplies [Section 17(1)/(2), Rule 42(1)(m)]

- Pro-rata reversal of ITC on capital goods put to other than business use or used for exempted outward supplies [Section 17(1)/(2), Rule 42(1)(h)]

- Short reversal on account of final determination of amount to be reversed under section 17(1) and (2) [Rule ITC 42(2)(a)]

Reclaim of ITC reversed would broadly include following situations:

- On account of final determination as above where excess amount has been reversed [Rule ITC-42(2)(b)]

- On account of amount paid subsequent to reversal of ITC

|

|

Amendment in respect of information submitted in earlier period in Table 11 can be made by furnishing revised information on selecting the relevant month in Table 11.

|

|

12

|

Levy-wise addition or reduction in output tax for mismatch and other reasons to be furnished in this table by the Taxpayer

Output Tax to be increased for following reasons:

- ITC claimed on mismatched Invoices or debit notes or duplication of invoices or debit notes

- Tax liability on account of mismatched credit notes

Output Tax to be reduced for following reasons:

- Reclaim on account of rectification of mismatched invoice/debit notes

- Reclaim on account of rectification of mismatched credit note

- Negative tax liability from previous tax period

- Tax paid on advance in earlier tax period and adjusted with tax on supplies made in current tax period

|

|

13

|

Reporting criteria for HSN shall be same as required in GSTR-1 wise value of outward supplies made during the period

|

FORM GSTR-3: RETURN BY A REGULAR TAXABLE PERSON

[Sec. 39(1), Rule 61]

- Every taxpayer furnishing details in Form GSTR-1 and 2 shall furnish a monthly return in Form GSTR-3

- Return to be furnished whether or not any supplies of goods or services have been made during a tax period [i.e., it is mandatory to file a NIL return]16

- Form 3B to be filed wherever due date for filing GSTR-1/ GSTR-2 has been extended [detailed in subsequent paras]

|

Table

|

Particulars

|

|

1

|

GSTIN of the taxpayer – Shall be auto populated on Login

|

|

2

|

Legal Name and Trade name of the taxpayer – Shall be auto populated on Login

|

|

PART-A

[To be auto-populated based on GSTR-1 AND GSTR-2]

|

|

3

|

Summary of values of outward supplies

[Taxable, Zero rated (tax paid), Zero rated (Others), Deemed exports, Exempted, Nil-rated, Non-GST supply]

|

|

4

|

Rate-wise details Inter-State supplies [Net Supply for the month17]

|

|

4.1

|

Details of Value and IGST/Cess in respect of

|

Cross referencing/ Remarks

|

|

Taxable Supplies [other than RCM and Zero rated]

|

Table 4A, 4C, 5, 7, 11 [GSTR-1]

|

|

Taxable Outward RCM Supplies18

|

Table 4B [GSTR-1]

|

|

Zero rated [IGST paid] supplies

|

Table 6, 11 [GSTR-1]

|

|

E-Commerce Operator wise summary of outward supplies made through it attracting TCS

|

Table 4C, 5B, 7B [GSTR-1]

|

|

4.2

|

Rate-wise details intra-State supplies [Net Supply for the month]

|

|

Details of Value and Tax19 in respect of

|

Cross referencing/ Remarks

|

|

Taxable Supplies [other than RCM]

|

Table 4A, 5, 7, 11 [GSTR-1]

|

|

Taxable Outward RCM Supplies

|

Table 4B [GSTR-1]

|

|

E-Commerce Operator wise summary of outward supplies

|

Table 4C, 5B, 7A [GSTR-1]

|

|

4.3

|

Tax effect of amendments made in respect of outward supplies

|

|

Details of Differential value and Tax in respect of

|

Cross referencing/ Remarks

|

|

(I) Rate-wise details of amendments relating to Inter-State Supplies

|

|

A. Taxable supplies [other than RCM/Zero rated]

|

Table 9, 10B [GSTR-1]

|

|

B. Zero rated [IGST paid] Supplies

|

Table 9A [GSTR-1]

|

|

C. Details of supplies through E-Commerce Operator [out of A above]

|

Table 9, 10B [GSTR-1]

|

|

(II) Rate-wise details of amendments relating to Intra-State Supplies

|

|

A. Taxable supplies [other than RCM]

|

Table 9, 10A [GSTR-1]

|

|

B. Details of supplies through E-Commerce Operator [out of A above]

|

Table 9, 10A [GSTR-1]

|

|

5

|

Inward supplies attracting reverse charge including import of services

[Net of advance adjustments]

|

|

5A

|

Inward Supplies on which tax is payable under RCM

|

|

Details of value and tax in respect of

|

Cross referencing/ Remarks

|

|

Ratewise details of inter-State Inward Supplies

|

Table 4, 10 [GSTR-2]

|

|

Ratewise details of intra-State Inward Supplies

|

Table 4, 10 [GSTR-2]

|

|

5B

|

Ratewise details of tax effect of amendments relating to inward RCM supplies

|

|

Ratewise details of inter-State Inward Supplies

|

Table 6, 10 [GSTR-2]

|

|

Ratewise details of intra-State Inward Supplies

|

Table 6, 10 [GSTR-2]

|

|

6

|

Input Tax Credit20

|

| |

Details of Taxable Value and Tax21 on inward supplies in respect of

|

Cross Reference/ Remarks

|

|

6(I)

|

Inward supplies received and Debit and Credit notes received during the month

|

Table 3, 4, 5, 6, 8 [GSTR-2]

|

|

6(II)

|

Amendments made to details of inward supplies furnished during earlier tax periods

|

Table 6 [GSTR-2]

|

|

7

|

Addition and reduction of amount in output tax for mismatch and other reasons

[To be auto-populated based on details furnished in Table 10 and 11 of GSTR-2]

|

| |

Description

|

Add to/reduce from output tax liability

|

Amount of Tax [Levy-wise]

|

|

(a)

|

ITC claimed on mismatched invoices/ debit notes or duplication of invoices/debit notes

|

Add

|

XXXX

|

|

(b)

|

Tax Liability on mismatched credit notes

|

Add

|

XXXX

|

|

(c)

|

Reclaim on rectification of mismatched invoices/Debit Notes

|

Reduce

|

XXXX

|

|

(d)

|

Reclaim on rectification of mismatch credit note

|

Reduce

|

XXXX

|

|

(e)

|

Negative tax liability from previous tax periods

|

Reduce

|

XXXX

|

|

(f)

|

Tax paid on advance in earlier tax periods and adjusted with tax on supplies made in current tax period

|

Reduce

|

XXXX

|

|

(g)

|

Input Tax credit reversal/reclaim

|

Add/ Reduce

|

XXXX

|

|

|

8

|

Summary of Taxable Value and Tax payable [Levy-wise] under the following heads:

- Outward Supplies

- Inward Supplies liable for payment of Tax under RCM

- ITC reversal/reclaim

- Mismatch, rectification, other reasons

|

|

9

|

Levy wise details of TDS and TCS Credit claim

|

|

10

|

Provides details of interest payable on account of various reasons [e.g. ITC mismatch, Delay in payment of tax]

|

|

11

|

Details of Late fee payable for compliance delay

|

|

PART B

[Details to be furnished by the tax payer]

|

|

12

|

Levy wise Details of tax payable and paid22

|

|

13

|

Levy wise details of interest and late fees payable and paid

|

|

14

|

Refund claimed from Electronic Cash Ledger23

|

|

15

|

Debit entries in electronic cash/Credit ledger for tax/interest payment [to be populated after payment of tax and submissions of return]

|

FORM GSTR 3B: SUMMARY RETURN IN LIEU OF MONTHLY RETURN

[Sec. 39(4), Rule 62]

Form GSTR-3B is a summary return and requires the taxpayer to provide summary details of output tax payable, input tax credit claimed, ineligible Input Tax Credit and net tax, interest, late fee payable and paid. Form GSTR-3B is to be filed whenever due dates for filing GSTR1 and GSTR-2 have been extended [Rule 61(5)]. Requirement for furnishing Form GSTR-3B has been notified for the months of July 2017 and August 2017 since due dates for filing of GSTR-1 and GSTR-2 have been extended. However, the taxpayer shall be subsequently required to file monthly returns in Form GSTR-3 for the tax period for which GSTR-3B is already filed

Summary of due dates for filing of Form 3B for July and August, 2017 have been tabulated here under:

|

Category of Taxpayer

|

Month

|

Due Date

|

Conditions, if any

|

|

Registered person entitled to claim transition credit in terms of section 140 but choosing not to file TRAN-1 on or before 28-08-2017

|

July 2017

|

25-8-201724

|

----

|

|

Registered person entitled to claim transition credit in terms of section 140 and filing TRAN-1 on or before 28-08-2017

|

July 2017

|

28-8-2017

|

•

|

Tax payable is paid on or before 25-08-2017

|

|

•

|

Form TRAN-1 is uploaded prior to filing Form GSTR-3B

|

|

•

|

If tax paid in cash

|

|

Any other registered person

|

July 2017

|

25-8-2017

|

—

|

|

All registered persons

|

Aug. 2017

|

20-9-201725

|

—

|

Details to be furnished in GSTR-3B are tabulated hereunder:

|

Table

|

Details to be furnished

|

Remarks/ Comments

|

|

3.1

|

Details of Outward Supplies and Inward Supplies liable for RCM

|

• This table provides for computation of gross tax liability of the tax payer on account of outward as well as inward RCM supplies during the tax period

• Total taxable value = Value of supplies + value debit notes – value of credit notes + value of advances received – value of advances adjusted against invoices raised in the current tax period

|

|

3.2

|

State wise details of Inter-State outward supplies made to unregistered persons, composition taxable persons and UIN holders

|

• State wise details to be furnished

• Total Taxable Value and IGST

|

|

4

|

Details of ITC claim for the tax period

|

|

(A)

|

ITC available on

|

|

|

(1)

|

Import of Goods

|

IGST ITC based on Bill of entry to be claimed

|

|

(2)

|

Import of Services

|

IGST based on Self Invoice generated by the taxpayer

|

|

(3)

|

Inward RCM supplies [other than 1 & 2 above)

|

ITC to be claimed on the basis of self invoice generated by the taxpayer

|

|

(4)

|

Inward supplies from ISD

|

—

|

|

(5)

|

All other ITC

|

This shall broadly include B2B inward supplies of goods and services against a Tax Invoice and on which tax has been charged

|

|

| |

|

|

(B)

|

ITC Reversals

|

|

|

(1)

|

As per Rule 42 & 43 of CGST Rules

|

ITC reversals to the extent it is attributable to supplies not liable for payment of GST or inward supplies put to other than business use

|

|

(2)

|

Other reversals

|

—

|

|

(C)

|

Net ITC available

|

Gross ITC – Reversals [A-B]

|

|

(D)

|

Ineligible ITC

|

|

|

(1)

|

As per Section 17(5)

|

Blocked credits to be mentioned here. These shall not be included in Part (A) above

|

|

(2)

|

Others

|

—

|

|

|

5

|

Values of exempt, Nil and non-GST inward supplies

|

The values need to be bifurcated into Inter-State and Intra-State

|

|

6.1

|

Payment of Tax

|

Details of how the gross tax under different levies has been paid by the taxpayer shall be furnished in this payment matrix table. Following points should be kept in mind:

- Order of utilisation of ITC available under various levies (IGST, CGST, etc.) in terms of Section 49

- Balance in e-Cash ledger under each of the levies can be used only for the payment of liability under the respective levy

|

|

6.2

|

TDS/TCS credit

|

Levy wise details to be provided

|

FORM GSTR-4: RETURN BY A TAXABLE PERSON OPTING FOR COMPOSITION UNDER SECTION 10

[Sec. 39(4), Rule 62]

- Furnish consolidated details of outward supplies on quarterly basis in common Form GSTR-4

- Furnish details of inward supplies on the basis of details contained in auto-drafted Form GSTR-4A in Form GSTR-4

- If the taxpayer opts out of composition at the beginning of the financial year he shall where required furnish details of inward and outward supplies relating to the period where he was not under composition26

- However, the taxpayer shall not be allowed to claim ITC in respect of invoices or debit notes pertaining to pre- composition period

- Similarly, once the taxpayer is out of the composition scheme he shall continue to furnish details relating to composition period in Form GSTR-4 (where required) till the due date for filing of return for the quarter ended Sep of the following financial year

|

Table 1

|

GSTIN

[auto-populated

on login]

|

Table 2

|

Name and Trade Name [Auto-populated]

|

Table 3

|

Aggregate Turnover of PY and Apr-June 2017

|

|

Details to be

furnished for

|

Table 4

|

Table 5

|

Table 6

|

Table 7

|

Table 8

|

|

Details of taxable inward supplies[including RCM supplies]

|

Amendments to details furnished in Table 3 [Including original/ revised debit and credit notes]

|

Rate wise details of Tax on outward supplies [Net of advances and goods returns]

|

Amendments to outward supply details furnished in Table 6 in earlier tax periods

|

Details of advances paid and adjustments for advances in case of inward RCM supplies [Including amendments thereto]

|

|

Details to be furnished for

|

Table 9

|

Table 10

|

Table 11

|

Table 12

|

Table 13

|

|

TDS credit received

|

Details of Tax Payable and paid

|

Interest, late fee payable and paid

|

Refund claimed in electronic cash ledger

|

Debit entries in cash ledger for tax/ interest [Populated on payment of tax and submission of returns]

|

FORM GSTR-5: RETURN BY A NON-RESIDENT TAXABLE PERSON

[Sec. 39(5), Rule 63]

Non-Resident taxpayers are required to furnish details of all taxable supplies in GSTR-5. Details to be furnished in GSTR-5 are tabulated hereunder:

|

Table

|

3

|

4

|

5

|

6

|

7

|

8

|

|

Details to be furnished for

|

Import of Inputs and Capital goods and ITC available

|

Amendments to Details submitted earlier in Table 3

|

B2B taxable outward supplies

|

B2C taxable inter-State outward supplies value > 2.5 lakhs

|

B2C taxable outward supplies [Net of Debit/ Credit Notes]

|

Amendments to details submitted earlier in Table 5 and 6

|

|

Table

|

9

|

10

|

11

|

12

|

13

|

14

|

|

Details to be furnished for

|

Amendments to details relating to supplies to unregistered persons submitted earlier in Table 7

|

Total Taxable value and tax payable on account of:

1) Outward Supplies

2) ITC mismatch

|

Tax Payable and Paid

|

Interest, late fee and any other amount payable and paid

|

Refund claimed from Electronic Cash ledger

|

Debit entries in electronic cash/ credit ledger for tax, interest payment [To be populated after filing of returns]

|

FORM GSTR-5A: RETURN FOR FURNISHING DETAILS OF SUPPLIES OF OIDAR27 SERVICES BY A PERSON LOCATED OUTSIDE INDIA TO A NON-TAXABLE PERSON IN INDIA

[Rule 64]

In case of OIDAR services, the person (service provider) located in non-taxable territory providing services to an unregistered person located in taxable territory, is liable for paying the IGST28. It is mandatory for such person to obtaining registration under the GST Law29 and furnish details of outward supplies in Form GSTR-5A

|

Table in GSTR-5A

|

|

1

|

2

|

3

|

4

|

5

|

5A

|

6

|

7

|

|

GSTIN

|

Legal name and Trade Name

|

Name of the authorised person in India

|

Period

|

Details of taxable outward supplies made to consumers in India [Place of Supply, Rate of Tax, Taxable Value, IGST, Cess

|

Amendments to details furnished in Table 5 in earlier period

|

Calculation of Interest, penalty or any other amount

|

Tax, Interest, late fees, any other amount payable and paid

|

FORM GSTR-6: RETURN FOR INPUT SERVICE DISTRIBUTOR [‘ISD’]

[Sec. 39(6), Rule 65]

Details of receipt of Tax Invoices and distribution of ITC shall be furnished by an ISD in Form GSTR-6 based on auto-drafted details provided in Form GSTR-6A.

|

TABLES

|

|

3

|

4

|

5

|

6

|

7

|

8

|

9

|

10

|

11

|

|

Input Tax credit received for distribution

|

Total ITC, eligible ITC and ineligible ITC [For e.g. Sec. 17(5)]

|

Distribution of eligible and ineligible ITC quoting GSTIN of the recipient unit and the State

|

Amendment in information furnished in Table 3, Debit/ Credit notes and amendments there to

|

ITC mismatches and reclaims to be distributed in the current month

|

Distribution of ITC reported in Table 6 and 7

|

Redistribution of ITC distributed to wrong recipient

|

Late Fees

|

Refund claimed from electronic cash ledger

|

FORM GSTR-7: RETURN IN RESPECT OF TAX DEDUCTION AT SOURCE [‘TDS’]

[Sec. 39(3), Rule 66(1)]

Under the GST regime certain specified persons are required to deduct Tax at Source on specified inward supplies received by them. TDS certificate is to be issued in Form 7A30. Further, details of amounts paid and Tax deducted are to be furnished in Form GSTR-7. Details to furnished are tabulated here under:

|

TABLES

|

|

1

|

2

|

3

|

4

|

5

|

6

|

7

|

8

|

|

GSTIN [shall be auto populated]

|

Name and Trade name [Shall be auto populated]

|

Details of GSTIN of the deductee, amount paid and levy wise TDS amount

|

Amendments to details furnished in Table 3 in earlier tax period and which needs correction

|

Amount of TDS and TDS paid

|

Interest and late fee payable and paid

|

Refund claimed from balance in

E-Cash ledger

|

Debit entries in electronic cash ledger for tax, interest payment

[To be populated after filing of returns]

|

Form GSTR-8: STATEMENT OF TAX COLLECTION AT SOURCE [‘TCS’]

[Section 52, Rule 67]

An e-Commerce operator is required to collect tax at source from net value of taxable supplies made through it. It has to furnish details of supplies made through it and the TCS in GSTR-8. Broad details furnished in GSTR-8 are as under:

|

Table in GSTR-8

|

|

3

|

4

|

5

|

6

|

7

|

8

|

9

|

|

GSTIN wise details of net supplies and TCS there on in respect of supplies made through the E-Commerce Operator

|

Amendments to details in Table 3 to be made through this Table

|

Details of Interest payable on delay in payment of TCS

|

Details of TCS payable and paid

|

Details of Interest payable and interest paid

|

Refund claimed from balance in Electronic Cash Ledger

|

Debit entries in electronic cash/ credit ledger [populated after filing of return]

|

Form GSTR-11: STATEMENT OF INWARD SUPPLIES BY PERSONS HAVING UNIQUE IDENTIFICATION NUMBER (UIN)

[Section 55, Rule 82]

Specialised agencies of the United Nations and other agencies are allotted a Unique Identification Number [‘UIN’] in lieu of a GSTIN31. Such persons are allowed to claim refund of taxes paid32 on the notified supplies of goods or services received by them. For claiming refund of the input taxes33 these persons are required to file a statement of inward supplies in Form GSTR-11. The refund is to be claimed by filing Form RFD-1034.

|

Table

|

Details to be furnished

|

Remarks/ Comments

|

|

1

|

UIN

|

Shall auto populate on login

|

|

2

|

Name of the UIN Holder

|

Shall auto populate

|

|

3

|

Details relating to the following are to be furnished:

- Invoice received during the tax period

- Debit/Credit notes received

|

Ratewise details to be furnished include:

- GSTIN of the Supplier

- Document details

- Taxable Value

- Levy wise tax amounts

|

|

4

|

Refund amount

|

- Levy wise details to be provided

- Bank details to be furnished

|

MISCELLANEOUS COMPLIANCES

Every RTP [Other than ISD, NR Taxable person, casual taxable person and persons liable for TDS/ TCS] shall file an annual return for every financial year on or before 31st December of following the end of the said financial year:

|

Provision

|

First return

|

Final Return

|

Annual return

|

|

Section

|

40

|

45

|

44

|

|

Form

|

----

|

GSTR-10

|

GSTR-9, GSTR-9A [Composition taxpayer], GSTR-9B [e-Comm]

|

|

Applicability

|

Every registered taxable person

|

Every Registered taxable person paying tax u/s. 9 and required to file return u/s. 39(1) and whose registration has been cancelled

|

Every registered taxable person other than the ISD, person paying tax u/ss. 51/ 52,

casual taxable person, NR taxable person

|

|

Compliance

|

Furnish details of outward supplies made between date he became liable for registration till the date of grant of registration

|

Furnish final return

|

1. Furnish annual return in prescribed form for every financial year

2. In audit cases [Section 35(5)] furnish audited accounts and reconciliation statement in GSTR-9C

|

|

Due Date

|

Normal Due date

|

3 months from date of cancellation or date of order of cancellation, whichever is later

|

On or before 31st December following end of the financial year

|

LATE FEE

[Sec. 47]

Section 47 provides for levy of late fee for default in furnishing of returns on or before the due date. Late fee shall be levied separately under CGST Act and respective SGST/UTGST Acts. The same are tabulated hereunder:

|

Nature of compliance

|

Nature of default

|

Amount of late fee

|

Maximum late fee

|

|

Furnishing of details required u/s. 37 or 38 or returns u/s. 39 or 45

|

Details or returns not furnished within due date

|

₹ 25 + ₹ 25 per day for monthly return

₹ 10 + ₹ 10 per day for quarterly return

|

₹ 5,000

|

|

Furnishing of annual return u/s. 44

|

Return not furnished within due date

|

₹ 100 per day

|

% of turnover in the State/UT

|

Late fees payable have been waived or modified by various notifications 4, 5, 6, 7/2018

MATCHING, REVERSAL AND RECLAIM OF INPUT TAX CREDIT

Section 41 states that a registered taxable person shall be allowed to self-claim ITC in respect of his inward supplies on provisional basis. This provisional acceptance shall be subject to the matching of claims in terms of section 42. In terms of section 42, all claims of ITC shall be matched by the GSTN portal after the due date of filing GSTR-3. The claims shall be matched –

- With corresponding details of outward supply furnished by the concerned supplier in the same or earlier month. Following details shall be matched:

- GSTIN of Supplier

- GSTIN of the Recipient

- Invoice or Debit note no.

- Invoice or Debit note date

- Tax Amount

- With the IGST paid on Import of goods by him

- For duplications of claims of ITC

Claims shall be accepted in following cases

- In respect of invoices and debit notes that were accepted by the recipient without amendments on the basis of GSTR-2A shall be accepted subject to the supplier filing a valid return;

- Where the amount of ITC claimed by the recipient is equal to or less than the amount of output tax paid by the supplier on such invoice or debit note. [Explanations 1 & 2 to Rule 69]

- Details of claims that have matched shall be communicated to the recipient in Form MIS-1 [Rule 70]

Discrepancy in ITC Claim

The matching process may lead to discrepancy on following broad grounds:

- Recipient has claimed ITC in excess of the tax declared by the supplier

- There is no matching declaration by the supplier

- Duplication of claim of ITC by recipient

Consequences in Case of Discrepancy

The discrepancy in ITC claim shall be communicated on GSTN portal to the recipient in [Form MIS-1] and supplier [Form MIS- 2] on or before the end of the month in which matching is done. This process may lead to the following situations:

|

Situation

|

Time of action

|

Consequence

|

|

Supplier rectifies the discrepancy

|

Adds or corrects details in GSTR-1 to be filed for the month in which discrepancy is communicated

|

ITC shall match and shall be allowed to the recipient

|

|

Recipient rectifies the discrepancy

|

Deletes or corrects details in GSTR- 2 filed for the month in which discrepancy is communicated

|

•

|

Recipient shall pay the unmatched amount

|

|

•

|

Interest to be paid u/s. 50(1)

|

|

Neither party rectifies

|

----

|

•

|

Addition of unmatched amount to output tax liability of the recipient in GSTR-3 for the month following the month in which discrepancy is communicated

|

|

•

|

Interest also shall be calculated u/s. 50(1)

|

|

Mismatch on account of duplication of claims

|

Addition in the month in which discrepancy is communicated

|

•

|

Addition to the output tax in the month of communication

|

|

•

|

Interest also shall be calculated u/s. 50(1)

|

|

Supplier subsequently makes a rectification

|

On or before the due date for filing of return for the month of September or second quarter of the following financial year or the actual date of furnishing of annual return, whichever is earlier

[Section 42(7) r/w S. 39(9)]

|

•

|

Recipient to reclaim as a reduction from output tax in GSTR-2

|

|

•

|

The interest paid earlier to be credited to the electronic cash ledger [Credit shall not exceed the amount of interest paid by the supplier]

|

GST AND ITS IMPACT ON ACCOUNTING

Accounting for GST is yet another challenge the businesses will have to accept so as to be ready for compliance in GST Regime.

The present article is divided into various segments to understand the impact of GST on the accounting aspects of businesses. Provisions under GST Act require maintenance of records, uploading information and/or periodic reporting and producing the same on demand.

Chapter VIII of the CGST Act contains provisions in respect of maintenance of accounting records. The Rules also provide for certain additional compliances and maintenance of documents.

|

Sr. No.

|

Information Categories

|

Requirements under GST

|

|

1

|

Basic records by all registered persons

|

In view of section 35(1), following records to be maintained:

|

| |

|

•

|

Production or manufacture of goods

|

| |

|

•

|

Inward and outward supply of goods or services or both

|

| |

|

•

|

Stock of goods

|

| |

|

•

|

Input tax credit availed

|

| |

|

•

|

Output tax payable and paid and

|

| |

|

•

|

Such other particulars as may be prescribed.

|

|

2

|

Additional requirements for all registered person

|

The rules also provide that the registered person shall keep and maintain records of:

|

| |

|

•

|

Goods or services imported or exported, or

|

| |

|

•

|

Supplies attracting payment of tax on reverse charge along with the relevant documents, including invoices, bills of supply, delivery challans, credit notes, debit notes, receipt vouchers, payment vouchers, refund vouchers and e-way bills

|

| |

|

•

|

Maintaining the record separately for each activity including manufacturing, trading and provision of services.

|

| |

|

•

|

Accounts of stock in respect of goods received and supplied; containing particulars of the opening balance, receipt, supply, goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples and balance of stock including raw materials, finished goods, scrap and wastage thereof.

|

| |

|

•

|

A separate account of advances received, paid and adjustments made thereto.

|

| |

|

•

|

Details of tax payable, tax collected and paid, input tax, input tax credit claimed together with a register of tax invoice, credit note, debit note, delivery challan issued or received during any tax period.

|

| |

|

•

|

Names and complete addresses of suppliers from whom goods or services chargeable to tax under the Act, have been received

|

| |

|

•

|

Names and complete addresses of the persons to whom supplies have been made

|

| |

|

•

|

The record should maintain audit trail in case of records maintained in electronic format

|

|

3

|

Service provider

|

•

|

Maintain records in respect of goods used in rendering of services, input service utilised and services supplied.

|

|

4

|

Works contract

|

Separate accounts for works contract showing:

|

| |

|

•

|

The names and addresses of the persons on whose behalf the works contract is executed

|

| |

|

•

|

Description, value and quantity (wherever applicable) of goods or services received for the execution of works contract

|

| |

|

•

|

Description, value and quantity (wherever applicable) of goods or services utilised in the execution of works contract

|

| |

|

•

|

The details of payment received in respect of each works contract and

|

| |

|

•

|

The names and addresses of suppliers from whom he has received goods or services

|

|

5

|

Log to be maintained

|

•

|

Any entry in registers, accounts and documents shall not be erased, effaced or overwritten and all incorrect entries and thereafter the correct entry shall be recorded

|

| |

|

•

|

A log of every entry edited or deleted shall be maintained

|

|

6

|

Records to be retained/preserved (Period)

|

•

|

Records in respect of invoices, bills of supply etc. have to be retained for a period of 72 months.

|

| |

|

•

|

Effectively, records are to be maintained for six years and nine months from the end of the year

|

| |

|

•

|

In case of matters which are pending in appeal or other proceedings, records are to be kept till the matters are settled plus a period of 1 year from the date of such orders

|

|

7

|

Agent & Principal

|

Every agent referred to in clause (5) of section 2 shall maintain accounts depicting the:-

|

| |

|

•

|

Particulars of authorisation received by him from each principal

|

| |

|

•

|

Particulars including description, value and quantity (wherever applicable) received or supplied on behalf of every principal

|

| |

|

•

|

Details of accounts furnished to every principal

|

| |

|

•

|

Tax paid on receipts or on supply of goods or services

|

|

8

|

Manufacturer

|

•

|

Shall maintain monthly production accounts showing quantitative details of raw materials or services used

|

|

9

|

Generation and maintenance of electronic records

|

•

|

Proper electronic back-up of records shall be maintained and preserved in case of destruction of such records shall be restored within a reasonable period of time

|

| |

|

•

|

On demand, the relevant records or documents shall be duly authenticated by him, in hard copy or in any electronically readable format

|

|

10

|

Owner or operator of godown or warehouse and Transporters

|

•

|

The transporters, owners or operators of godowns, if not already registered under the GST Act(s), shall submit the details regarding their business electronically on the Common Portal in FORM GST ENR-01

|

| |

|

•

|

Business of transporting goods shall maintain records of goods transported, delivered and goods stored in transit by him and for each of his branches

|

| |

|

Owner or operator of godown or warehouse shall maintain books of accounts with respect to:

|

| |

|

•

|

The period for which particular goods remain in the warehouse, including the particulars relating to dispatch, movement, receipt, and disposal of such goods.

|

| |

|

•

|

The goods shall be stored in such manner that they can be identified item wise and owner wise and shall facilitate any physical verification or inspection, if required at any time.

|

|

11

|

Reconciliation Statements (Hidden requirements)

|

a)

|

Reconciliation of financial records maintained at GSTN portal:

|

| |

|

|

- Dispatches to/from branches, addition and disposal of assets etc. are also added to the aggregate supply. In the circumstances, there would be differences between financial books of account and the ‘aggregate turnover’ reported in GSTR-1.

|

| |

|

|

Typically, the credit reversed on account of mismatches, orphaned entry or non-payment to vendor will get reflected only on the GSTN portal; however, in the financial books these items will continue as claimable credits.

|

| |

|

b)

|

Reconciliation of GSTR with the financial/MIS reports:

|

| |

|

|

- Aggregate of the turnover of sales as per particular HSN code should tally with the sales reflected of bulk drug in the financial accounts.

|

|

12

|

IT system

|

Accounting challenges which require attention and IT support are highlighted as under:

|

| |

|

•

|

Linkages of debit note/credit note with original invoices

|

| |

|

•

|

Adjustment of advance received against a supply and tracking of receipt voucher and payment voucher

|

| |

|

•

|

Monitoring and verification of ITC reversal

|

| |

|

•

|

Statistical information in respect of number of invoices raised during the period

|

| |

|

•

|

Creating and updating product master and service master with the respective HSN/SAC codes

|

| |

|

•

|

IT software should prompt an alert or determine the ‘place of supply’ [POS] and ‘location of supplier’ [LOS] so that errors in determining intra-State or inter-State supplies is eliminated/minimized

|

| |

|

•

|

The delivery challan may have cross reference of invoice number

|

| |

|

•

|

The invoicing/accounting software should have built in rule/concept to determine the following:

|

| |

|

|

- Inter-State and intra-State

- Location of supplier, and

- place of supply

for different types of supplies

- Rate of tax

- HSN or SAC code classification

- Composite supply

- Mixed supply

- RCM – inward supply

- LOS and POS thereof

- Rate of tax

- Claim of ITC

- Creation of payment voucher

- Reporting

- Bill-to ship-to type of transaction

- POS and LOS thereof

- HO placing order on behalf of branch factory etc. – generation of document and recognising of the tax liability

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

13

|

Chart of Accounts

|

Under GST all these taxes (excise, VAT, service tax) will get subsumed into one account, and following new accounts have to be created:

|

| |

|

•

|

Input CGST a/c

|

| |

|

•

|

Output CGST a/c

|

| |

|

•

|

Input SGST a/c

|

| |

|

•

|

Output SGST a/c

|

| |

|

•

|

Input UTGST a/c

|

| |

|

•

|

Output UTGST a/c

|

| |

|

•

|

Input IGST a/c

|

| |

|

•

|

Output IGST a/c

|

| |

|

•

|

Electronic Cash Ledger (to be maintained on Government GST portal to pay GST)

|

| |

|

•

|

Electronic Credit Ledger (to be maintained on Government GST portal to pay GST)

|

| |

|

•

|

Electronic Liability Ledger (to be maintained on Government GST portal to pay GST)

|

| |

|

It may be noted all these records are to be maintained State wise, hence if a person is having registration under the GST Act, say in five States, the above chart of accounts need to be multiplied by five times.

|

ACCOUNTS TO BE MAINTAINED UNDER GST REGIME

To summarise, every registered taxable person shall keep and maintain, at his principal place of business, a true and correct account of production, inward and outward supply and such other records as specified under Goods and Services Tax Act.

|

Accounts / Records

|

Information required

|

By whom?

|

|

Register of Goods Produced

|

Account should contain detail of goods manufactured in a factory or production house

|

Every assessee carrying out manufacturing activity

|

|

Purchase/Inward Register

|

All supplies received during each tax period for manufacturing/sale/supply of goods and/or services

|

All Assessees

|

|

Sales/Outward Register

|

Account of all the supplies made whether of goods or services during each tax period

|

All Assessees

|

|

Stock Register

|

This register should contain a correct record of inventory available at any given point of time.

|

All Assessees

|

|

Input Tax Credit Availed

|

This register should contain the details of Input Tax Credit availed in each tax period

|

All Assessees

|

|

Output Tax Liability

|

This register should contain the details of GST liability in respect of al taxable supplies with reference to rate of tax

|

All Assessees

|

|

Output Tax Paid

|

This register should contain the details of amount paid as CGST, SGST and IGST, each tax period wise

|

All Assessees

|

|

Other Records as may be specified

|

Government can further specify, by way of a notification, additional records and accounts to be maintained

|

Specific Business as may be notified by the Government

|

Services Accounting Code

All invoices raised need to mention the Harmonised System of Nomenclature (HSN) Code as under:

|

Sr. No.

|

Annual Turnover in the Preceding Financial Year

|

Number of digits of HSN code to be mentioned in the Invoice

|

|

1.

|

Up to ₹ 150.00 lakhs

|

Nil

|

|

2.

|

More than ₹ 150.00 lakhs and up to ₹ 500.00 lakhs

|

2

|

|

3.

|

More than ₹ 500.00 lakhs

|

4

|

- Monthly return for aggregate turnover exceeding ₹1.5 crore. Quarterly returns for the other RTPs 57/2017

- Due date for filing GSTR has been extended or newly notified videnotifications 18, 20, 21, 26, 27, 35, 56, 72/2017; 2/2018 [Latest Notifications must be checked to comply with the due dates]

- Form not applicable till GSTR for period ending June 2018

- In case of expiry of validity of registration return to be filed within 7 days of expiry of registration

- Applicable in cases where aggregate turnover of the taxpayer exceeds ₹2 crore

- This table would contain details of the taxpayer’s outward supplies where the recipient/ client is required to discharge tax under RCM

- The GSTIN should be an active TIN as at the date of the invoice

- Invoice Value means net value plus tax charged

- Section 16 IGST Act, 2017

- Section 147

- Values shall be provided net of Debit/ Credit notes

- Separate tax amounts for IGST, CGST, SGST/UTGST, Cess shall be provided

- Whereever it is possible to do so at invoice level

- Bill of Entry number shall be the 6-digit port code + bill of entry number [Total 13-digits]

- Due to Credit note issued by a supplier to the ISD. This implies that the amount of credit note is in excess of the amount of credit to be distributed

- Section 39(8)

- The values and tax shall include value and tax payable on advances and net of adjustments made in respect of advances during the tax period

- Tax on these supplies shall be payable by the recipient of the taxpayer

- CGST, SGST/UTGST, Cess

- ITC on inward taxable supplies, including imports and ITC received from ISD

- IGST, CGST, SGST/UTGST, Cess

- Taxpayer is expected to provide details of mode of payment of liability [Cash/Credit] based on which debit entries shall be paid in the respective ledgers

- Any excess amount of balance in electronic cash ledger can be claimed by the taxpayer by providing details in this Table

- Due date for filing of GSTR-3B was extended videNotification No. 24/2017-Central Tax, dated 21-8-2017. The due date was earlier extended vide Notification no. 23/2017-Central Tax, dated 17-8-2017 which amended the original due date notified videnotification no. 21/2017-Central Tax, dated 8-8-2017

- Notification No. 21/2017-Central Tax, dated 8-8-2017

- Rule 62(4)

- OIDAR – Online information or data access or retrieval service

- Section 14 of the IGST Act, 2017

- Section 24(xi)

- Rule 66(3)

- Section 25(9)

- Refund shall be available only in case of inward supplies received from registered persons against a tax invoice and the price of the supply covered by a single tax invoice is greater than ₹5,000 [Rule 95(3)]

- Section 55

- Rule 95(1)

Back to Top

|