BCAS President CA Zubin Billimoria’s Message for the Month of April 2026

My Dear BCAS Family,

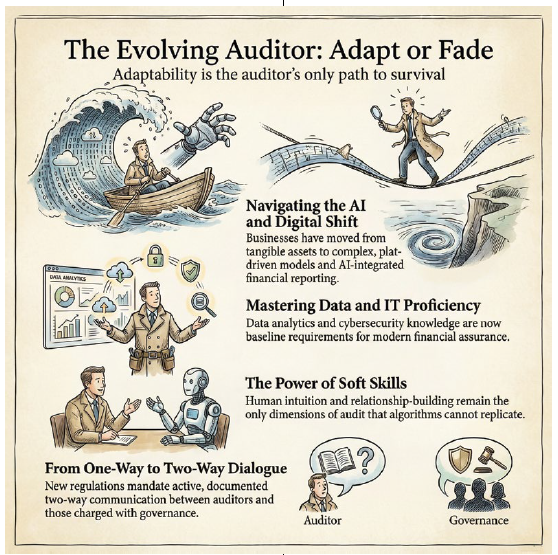

As I start to pen my thoughts, another financial year has ended. This has prompted me to reflect on how the audit profession is keeping pace with the rapidly changing landscape, in which the businesses we audit are no longer confined to tangible assets and predictable revenue streams. We now navigate complex financial instruments, platform-driven business models, increasingly intricate related-party structures and the emerging frontier of ESG and sustainability reporting, where assurance standards are still taking shape. Are we, as a profession, truly keeping pace with the world we are being asked to audit?

Further, technology, primarily driven by AI, is bringing about a tectonic shift in the audit profession. Finally, communication has always been a major pillar of the audit profession, be it in the form of the Audit Report, communication to Those Charged With Governance (TCWG), Engagement team discussions and Audit Documentation, is under greater public scrutiny by various stakeholders and regulators, thereby changing its role and importance.

Accordingly, I feel it is appropriate to discuss the themes of Upskilling and Communication and their roles within the audit profession’s changing dynamics.

UPSKILLING – AN ESSENTIAL IMPERATIVE OF THE AUDIT PROFESSION

Audit, over the years, has been rooted in processes such as planning, execution, and reporting, which require skills such as professional scepticism, technical accounting knowledge, an understanding of internal controls, auditing standards, and relevant laws and regulations. How we apply these processes has drastically transformed over the past few years and we have not seen the last of it.

Some of the important changes like automation of routine work, increasing volume and complexity of data, emerging areas like cyber security and IT audit and the ever-expanding and complex regulatory environment, demand increasingly specialised skill sets which were not the core competency of the profession.

While each of these changes may not represent an immediate threat to the profession, they make it imperative for the auditor to upskill to remain relevant. Further, upskilling cannot be achieved by attending seminars alone; it requires a conscious effort to acquire new capabilities that enable auditors to add greater value and improve the quality and delivery of services. Though the list of areas where upskilling is required is unlimited, the following are, in my view, certain critical domain skills which auditors need to acquire.

Data Analytics: Proficiency in data analytics tools, whether it is Excel or at a more sophisticated level like Power BI, Python, etc., is now a baseline expectation rather than a distinguishing skill. It helps structure and interrogate large datasets, identify anomalies, and provide insightful analysis well beyond routine compliance verification.

Technology and IT Audit: Every auditor working with technology-dependent organisations, which are now predominant, needs knowledge of cloud architecture, application controls, access management, and cybersecurity controls to analyse their impact on financial reporting risk. Certifications such as DISA and CISA, as well as courses offered by ICAI’s Digital Accounting and Assurance Board (DAAB), are valuable starting points.

Soft Skills: As transactional and compliance work becomes more automated, the distinctively human dimensions of the audit relationship assume greater importance. The ability to communicate complex findings in plain language, provide constructive guidance, and build trusted relationships at the board and audit committee levels is a skill no algorithm can replicate.

This brings me to the role of communication within the changing audit paradigm.

CHANGING ROLE OF COMMUNICATION FOR THE AUDIT PROFESSION

The audit profession today operates in an environment of remarkable complexity. The rise of data analytics, artificial intelligence, and blockchain has altered not only how audits are conducted but also what auditors are expected to know and convey. The advent of real-time reporting means that stakeholders no longer wait for an annual report; they expect continuous, transparent, and digestible financial intelligence. These changes demand a corresponding evolution in how auditors communicate.

A few of the relevant changes are as follows:

Changing Architecture of the Audit Report: The traditional audit report, has evolved from a boilerplate template, to include Key Audit Matters, enabling focused communication between the auditors and financial statement users by highlighting areas of significant judgment and estimation, as well as the procedures followed to address them.

Communication to Those Charged with Governance (TCWG): While Standards on Auditing always dealt with this topic, the expectations of Boards, Audit Committees and Management have increased in the recent past with greater expectations of conversations around internal control weaknesses, going concern assessments, fraud risk, management estimates and judgements, related party transactions, etc. Further, the recent circular dated 7th January, 2026, issued by NFRA mandates a two-way communication process, as opposed to the one-way process from the Auditors to the Audit Committee and TCWG, which had been the general norm. Accordingly, commencing from 1st April, 2026, Boards would have to clearly define who would be considered as TCWG and also document an overall communication framework between TCWG and auditors.

Technology and Digital Communications: Digital communication channels like email, video calls, and other digital platforms have transformed the nature of communication, making it more informal, thereby challenging audit documentation in terms of the SAs. Further, the use of AI-driven audit tools and their algorithmic opacity, together with cyber breaches and data privacy considerations under the recently enacted DPDP Act, pose new challenges and limitations for auditors’ client communications.

ROLE OF BCAS

Over the past seven decades, BCAS has supported various capacity-building initiatives, focusing on programmes on emerging and contemporary topics, as well as advocacy and research initiatives such as the recent research paper on Global Taxation. The recent lecture by CA Nawshir Mirza, “Auditors Expectations from Audit Committees,” could not have been more timely in the context of the NFRA circular referred to above. Our mentorship programmes also establish a cross-generational communication channel.

Adaptability is Non-Negotiable

To conclude, I would like to refer to the famous quote by the naturalist and scientist Charles Darwin in the context of the transformation driven by AI and digital transformation, making it imperative for the audit profession to adapt continuously.

“It is not the strongest of the species that survive, nor the most intelligent, but one most responsive to change”

A big thank you to one and all!